How Tracking My Expenses (Almost) Helps Me Sleep Better

Introduction

Dear readers, I realised early on that I needed to work on my personal finance literacy. One concept that kept appearing everywhere was budgeting. So I decided to embark on a long-term pursuit of understanding and managing my own funds.

But as soon as the salary got credited into my account and the outflow of money began, I had no mechanism to understand where those funds were going. This lack of visibility brought uncertainty — and with uncertainty, it was hard to plan or make confident decisions. Not going to lie, at times that uncertainty became a source of mild worry.

Everything changed when I started tracking my expenses. This isn’t a how-to post. But if any part of this sounds familiar, or if you’ve ever wondered where your money disappears every month, you might find this perspective worth reading.

The Problem

Like most people, right after payday, the usual cycle began — expenses flowing out little by little. But every now and then, usually during lunch breaks, while commuting, or towards the month’s end, a few questions would pop into my head:

- Where exactly is my salary being spent?

- What are the common types of expenditures?

- In case of an emergency or cost-cutting, which expenses can I reduce or postpone?

Without data, these questions were impossible to answer accurately. Relying on memory was unreliable at best. It soon became clear that the real problem wasn’t overspending — it was not knowing where the money was going. I was spending, but I couldn’t trace the flow. Without that visibility, even the most basic analytical questions about my habits were left unanswered.

The Mindset

More than anything, I consider myself a student of problem-solving. So, when this challenge appeared, I saw it as an opportunity to apply that mindset to my own life — to create something useful and measurable.

Before answering any financial questions, I needed data. Once I had data, I could analyse spending patterns, derive insights, and even make inferences about future behaviour — essentially, small-scale predictions.

I chose discipline over motivation as the foundation of this system. Because honestly, my motivation sometimes has a shorter lifespan than the half-life of the most radioactive isotopes.

To make the system sustainable, I defined three non-negotiables and followed them strictly for the past 12 months without fail:

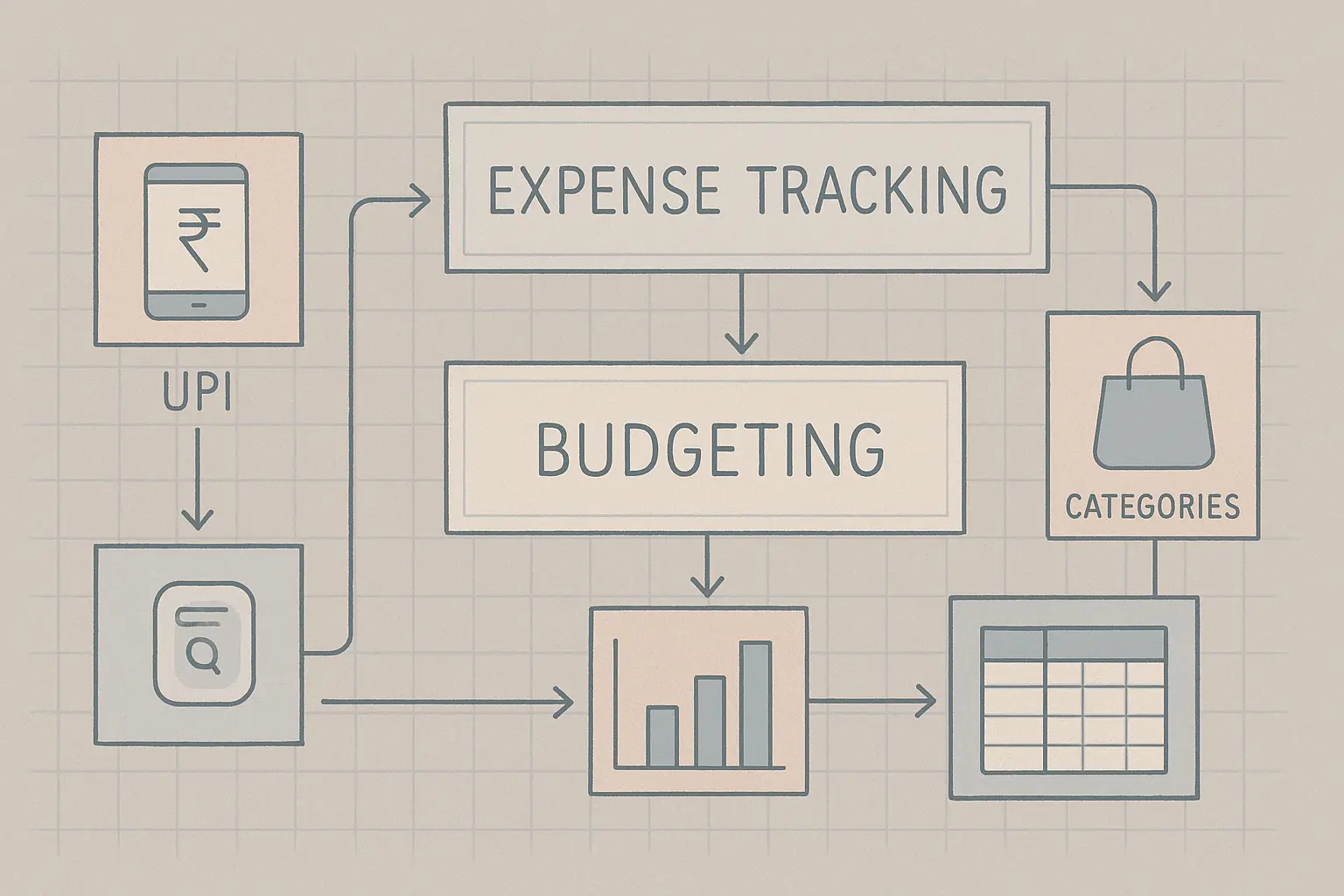

- Make all transactions via UPI for clean, granular tracking.

- Maintain common categories for all expenditures.

- Record every transaction of the day in a Google Sheet before sleeping.

Analytics and inference rely on historical data — and to have historical data, one must track the present.

The System

Let’s get a bit technical. The entire process runs through Google Sheets. It’s not an industry-grade setup, but it solves my specific problem effectively.

- Master Categories — a sheet with canonical categories like essential_groceries, luxury, rent, subscriptions, office_travel, personal_travel, etc.

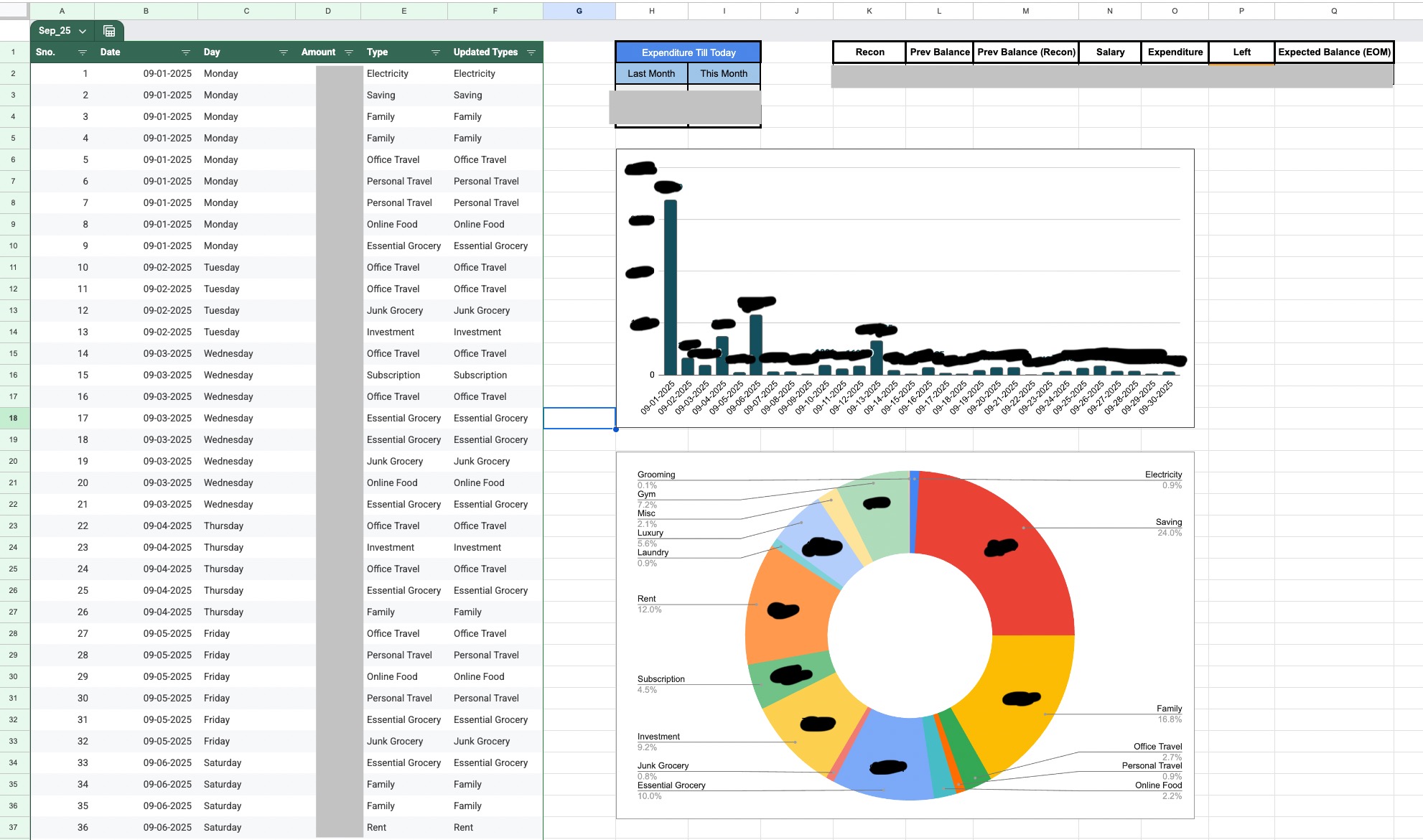

- Monthly Expenditure — each month has its own sheet (e.g., dec_24, jan_25) with columns: Date, Day, Amount, Type, Updated Type. "Updated Type" is synced from the master categories table.

- Current Month Forecast — category-wise averages from past months, dedicated amount (upper limit), spent, spent/day, left, and left % with a colour-coded indicator.

- Monthly Dashboard — pivot-like summary of category totals per month and averages for trend tracking.

- Moving Averages — 3-month moving averages per category to help forecast and measure forecast error.

Insights and Decision-Making

Once the system was in place, the data began revealing patterns — not just about spending, but about behaviour. Over time, I learned two key aspects of reading this data:

- Understanding my behaviour — recognising how and why I spend.

- Shaping future decisions — adjusting allocations for smarter financial control.

Some questions I can now answer confidently:

- How much do I typically spend on essential groceries each month?

- Which expenses can I reduce when I want to build a buffer?

- Why did I overspend on "luxury" in certain months — one-offs or poor estimates?

- Which categories remain consistent regardless of total spend?

- In case of an emergency, how long can I survive comfortably with current savings and expense cuts?

These insights have turned my anxiety into confidence. Earlier, seeing my balance dip by the 20th of the month used to make me uneasy. Now, it doesn’t. I know what “low” truly means, and I trust the system enough to know that every number is accounted for. Even months with higher expenses — like my birthday or Diwali — now feel completely under control.

I got 99 problems, but my expenses ain’t one.

Final Thoughts

If you’ve made it this far, thank you for reading. It means you either share an interest in personal finance or you’re simply curious to see how someone else manages theirs. Either way, I hope this gave you a new perspective.

This wasn’t meant to be a step-by-step guide — just my take on expense tracking and the peace of mind it’s brought me. It’s also a small side project. Someday, once it matures, I might turn it into a web or mobile app.

This is me, Adil, signing off.